Social:

|

|

||

|

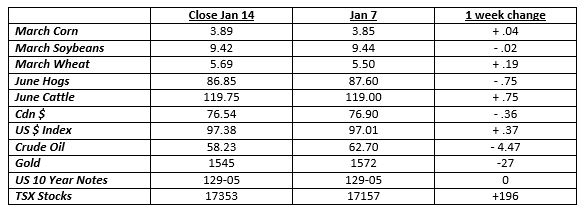

Grain prices were mixed again over the past week. Wheat was by far the strongest on technical buying. The continuation charts are at their best level since August 2018, and not far from its best level in 4 1/2 years, when futures last traded at $6.00

The highly anticipated USDA report released Jan 10 turned out to be a dud. While the numbers were mostly bearish, prices refused to break down. This is usually a positive for price when that happens.

Grain stocks at December 1 were a bit of a positive surprise, and all less than a year ago at the same time. Corn is down 548 mln bu., compared to Dec. 1, 2018 and 83 mln less than traders thought.

Soybean stocks are down 494 mln bui compared to a year ago, but at 3.252 bln bu, is more than expected. Wheat stocks at Dec. 1 were as expected at 965 mln bu, down 115 from a year ago.

US yield estimates were bearish. Corn was raised 1 bu/ac from the Dec. report to 168 bu. Traders expected 166. Soybeans were pegged at 47.4 bu, up .5 from Dec. and .9 from pre-report guesses.

Final carryout guesses for the 2019/20 crop were higher than expectations because of the higher yields, but were tempered by the smaller Dec. 1 stocks. The bottom line is that carry outs are falling in all crops, which is a positive.

US winter wheat seedings were put at 30.80 mln., the lowest in over 100 years. However, soft red wheat acres were 550,000 more than traders thought. Since Ont mainly grows soft red, the report isn’t as friendly to our soft red basis as it could have been.

Tomorrow is finally the signing of Phase 1 of the US/China trade agreement. This is an anticipated event, as tariffs and negotiations have been going on since March, 2018, so markets are not responding to the actual signing.

Hopefully some specific details will come out shortly. There is no doubt China will import more US ag products, but that too has been widely discussed. Hopefully China will adhere to whatever they sign.

Agriculture has been hurt by Trump’s tariffs likely more than any other industry. Hopefully the trade deal will help the US get back some of the market share that they lost during the process.

China buying more US ag products could cause the US to lose some of the markets they have with all their other customers, who may now have to go elsewhere for their needs. World demand is relatively static, so the trade deal is more of a shift in demand than new demand.

Frank Backx |

||

|

||

|

||

|

|

|

Marketing & Communications 34 July 16, 2026 |

|

|

Hensall Co-op 323 April 8, 2026 |

|

|

|

Crop Services 22 April 2, 2026 |

|

|

|

Energy Division 4 February 1, 2022 |

|

|

|

Membership Office 1 July 3, 2020 |