Social:

|

|

||

|

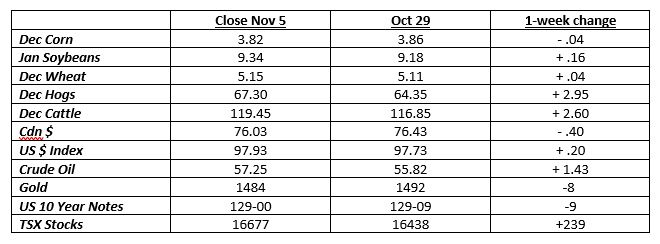

Soybeans and wheat were a bit firmer over the past week, while corn weakened. There was little in the news to create excitement or disappointment. Large speculator buying was the main impetus for the soybean rally.

In the latest week, they bought another 5500 contracts, to be long 72,300. That is their largest long position since June 2018. Large specs remain short the corn and wheat markets

Harvest is proceeding, and now 52 percent of the corn has been harvested, while 75 percent of the soybeans are in bins. This is still behind the 75 and 87 percent respectively that is normal for this time of year.

October marked the 15th straight month in which precipitation was greater than the long-term average in the Midwest. This is thought to be a record. This is obviously OK during the growing season but is not ideal during planting or harvest. Ontario harvest progress remains slow. There’s still a lot of soybeans out in fields and corn combining has only just begun in a few areas. The colder temperatures in the forecast could actually be beneficial, especially in the wetter areas.

South America is expected to see normal to above rainfall for the next 2 weeks. This will alleviate any concerns about it being too dry to plant. The best hope for a significant rally in grains would be from dry weather in the southern hemisphere.

The other short-term fundamental bit of news will come out on November 8, when the USDA releases its monthly demand/supply report. Not a lot of change in yield is expected compared to the October version. Corn usage could be lowered, however.

Nothing concrete happened with the trade war. Again, it was all rumours and speculation. However, China has been a much larger buyer of soybeans from the US over the past 6 weeks. China is usually a buyer from US sources at harvest time.

Last week, the US Federal Reserve dropped its short-term interest rate 25 basis points, while the Bank of Canada kept our rates steady. Logic says this should have supported our dollar, but it didn’t. Canada now has the highest interest rates in the G7.

|

||

|

||

|

||

|

|

|

Marketing & Communications 34 July 16, 2026 |

|

|

Hensall Co-op 323 April 8, 2026 |

|

|

|

Crop Services 22 April 2, 2026 |

|

|

|

Energy Division 4 February 1, 2022 |

|

|

|

Membership Office 1 July 3, 2020 |