Social:

|

|

||

|

Last Monday’s US corn crop ratings report was a bit of a surprise as 3% fell out of the good or excellent categories to only 55% now. Last year it was 68% at this time. Illinois showed the largest drop, falling 8 point to only 38%. The US corn crop remains well behind in maturity. Only 55% is dented. Last year it was 84%, while the average for this date is 77%. A large portion of the crop needs a lot more time to finish.

Only 92% of US soybeans are setting pods. That means over 6 million acres are not, or about twice the total acres planted to soybeans in Ontario. An early frost would obviously be devastating to the soybean crop also.

Ontario corn and soybean fields are also late, with a huge variability in crop conditions even in a small area. Overall yields are unlikely to be as strong as they have been in the past 2 to 3 years. Unfortunately, prices don’t look like they will make up for the smaller crops.

USDA will release their monthly demand/supply report on September 12. Most are looking for a slight reduction in yield compared to their August report. The other important component is acres. Will USDA acknowledge the acres not planted? Brazil usually starts planting their soybeans by mid September. Conditions there are very dry for this time of year, so very little planting is occurring. However, Brazil has a very wide planting window, so markets aren’t concerned yet.

Wheat prices firmed when Australia predicted their wheat crop would only be 19.2 million mt. USDA has them at 21 mln, which is still well below the 25 mln mt average they have achieved over the past 5 years. This should help North American exports.

Livestock markets remain on the defensive. Cheap grain usually leads to cheaper meat prices, as farmers walk the grain off the farm. Cattle hit a 10-year low in the latest week. Seasonals are usually weak heading into the fall.

Outside markets were mixed. Recessionary fears linger, keeping a lid on interest rates. The low rates and amount of liquidity in the system is keeping stock markets firm, however, as all the savings etc. need to have a home. |

||

|

||

|

||

|

|

|

Marketing & Communications 34 July 16, 2026 |

|

|

Hensall Co-op 323 April 8, 2026 |

|

|

|

Crop Services 22 April 2, 2026 |

|

|

|

Energy Division 4 February 1, 2022 |

|

|

|

Membership Office 1 July 3, 2020 |

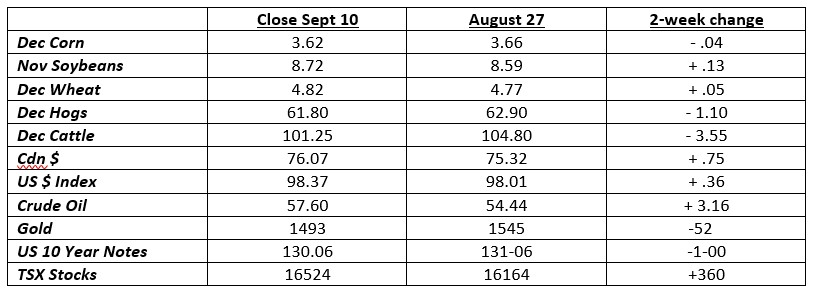

Prices were mixed over the past 2 weeks. Weather remained non-threatening. A warm, wet 2-week forecast will add bushels and help crops reach maturity. There is no risk of frost in any of the main growing areas.

Prices were mixed over the past 2 weeks. Weather remained non-threatening. A warm, wet 2-week forecast will add bushels and help crops reach maturity. There is no risk of frost in any of the main growing areas.