Social:

|

|

||

|

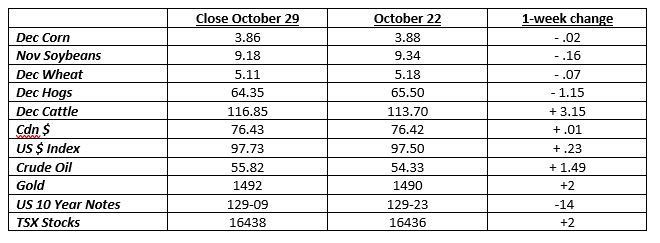

Prices were lower over the past week, led by soybeans. Often the last part of harvest can cause price weakness. Slow corn exports and ethanol grind aren’t helping that market either.

US corn is 41 percent in the bin. Normally it is 61 by now. Soybean harvest is also lagging at 62 percent, 16 percent behind the average pace.

October has been uneventful, pricewise. Corn has been confined to a 20-cent range for the month. Soybeans have had a 35-cent range, while wheat has traded between $4.85 and 5.35.

Ontario basis levels are as dormant as futures, even though our dollar rose a cent and a half since early in the month. Strong US basis values are supporting our basis here, as US grain companies bid up for the smaller crops.

Large speculators don’t hold any extreme positions in the grains. They are short corn (32,900 contracts) and wheat (12,300 contracts). They are long a relatively small 35,700 soybean contracts.

Soybean harvesting in Ontario is wrapping up. Yields are highly variable, but overall are expected to be less than the past 2 years. There will be very little corn off before November starts, with more rain in the short-term forecast.

The China/US trade war is still very much in the news. Supposedly, Phase 1 is to be signed Nov 17, but don’t hold your breath on that one. There have far too many false alarms already, and what exactly is in Phase 1?

South America is getting more rains, which will help with their soybean planting. Periodic rains later are more critical later when plants are in their vegetative and reproductive stages, as their soils tent to be course.

There wasn’t much movement in other markets either. It’s getting tougher and tougher to write about markets when, so little is happening. Perhaps it’s just the calm before the storm?

|

||

|

||

|

||

|

|

|

Marketing & Communications 34 July 16, 2026 |

|

|

Hensall Co-op 323 April 8, 2026 |

|

|

|

Crop Services 22 April 2, 2026 |

|

|

|

Energy Division 4 February 1, 2022 |

|

|

|

Membership Office 1 July 3, 2020 |