Social:

|

|

||

|

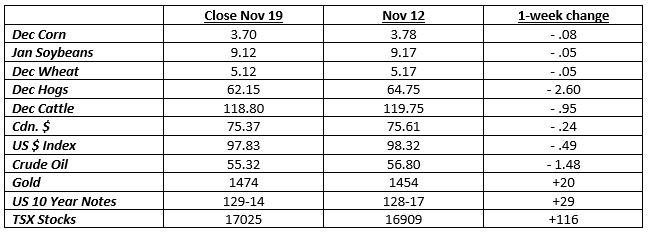

Grain prices remain in the doldrums, with prices losing more ground in the past week. Corn is now near its worst level in Chicago in 2 months, while soybeans trade at a 1 ½ month low. This isn’t unusual seasonally, as the US nears the end of harvest.

Corn is now 76 percent harvested, up 10 percent in the past week, but still behind the average pace of 92 percent. Soybeans are 91 percent in bins, up 6 from last week. Usually, by now 95 percent are off.

The Ontario corn and soybean harvests are further behind than that in most of the US. Corn is drying down at a slow rate, which isn’t unusual for this time of year. The recent wet weather and damp forecasts obviously won’t help that situation either.

China has resumed poultry imports again from the US. The week before, they announced they were going to increase meat imports from Canada also. They need more meat protein as they deal with the African Swine Fever that has decimated their hog numbers.

Despite these announcements, US livestock futures weakened. Cheap grain prices throughout the world are giving incentives for producers to increase their herds. Eventually, this will increase feed demand, but it is a slow process.

South America is expected to see regular rainfall over the next week or two. This is also contributing to the lower prices in Chicago. Some areas in the south are dry. December and January weather will determine their crop sizes.

US exports of grain have been poor lately, due to the ongoing trade war and stiff competition from other sellers, such as Russia. However, international prices are firming, which should allow the US to get back some of the customers they lost.

Outside markets also remain quiet for the most part. US stocks again traded at new record highs. There seems to be some disconnect between main street and Wall Street. Other than employment, most economic indicators aren’t firing on all cylinders.

With interest rates still near record lows, investors keep putting more dollars into stock markets. The major US stock indices are up over 20 percent again in 2019. Because the trend has been up since the recession low in 2009, the rally is long in the tooth by historical standards.

As in all markets, though, the trend is your friend.

|

||

|

||

|

||

|

|

|

Hensall Co-op 299 June 25, 2025 |

|

|

Marketing & Communications 18 June 24, 2025 |

|

|

|

Crop Services 21 September 27, 2024 |

|

|

|

Energy Division 4 February 1, 2022 |

|

|

|

Membership Office 1 July 3, 2020 |